“The cash wedge.” At first glance, it seems like a strange term. It sounds like a physical pile of cash that’s used to wedge something up.

Now here’s why it’s actually a great term: that’s exactly what it is, only it’s not a physical pile of cash. It has more to do with the liquidity of your investments and your ability to sell assets without losing market value.

Here’s a quick look at what this strategy entails — and why we use it with many of our clients.

What is the cash wedge strategy?

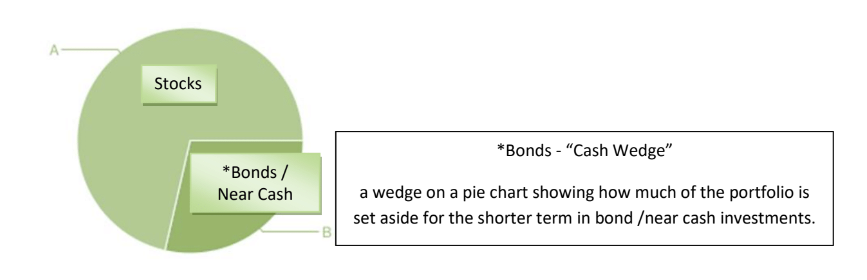

Imagine all of your investments and savings as a circle or pie chart. Within this circle are all of your mutual funds, stocks, bonds, GICs, high-interest savings, and any other investment you may have.

The cash wedge strategy separates your stocks from your more liquid investments. It’s a “wedge” or piece of the pie. This wedge is made up of assets like bonds and less volatile investments. The amount in the wedge is calculated by estimating the amount of money each client needs within three to seven years (depending on personal circumstances). Income from the cash wedge can be safely withdrawn, while the larger portion of the portfolio invested in stocks can continue to grow.

Why use the cash wedge strategy?

The cash wedge strategy is one that we like to use for many of our clients, especially when it comes to saving for retirement, for a child’s post-secondary education or for any significant purchases that may come up in the short term. This is because it helps us manage risk and keep our clients’ income safe during market downturns or recessions.

Stocks are an excellent investment tool, but they’re a much more volatile asset, often fluctuating in value. They’re typically best used for long-term investing over a period of eight years or longer.

Taking income from a volatile asset like stocks should be avoided to maximize long-term gains. Having a cash wedge of liquid or near cash funds available prevents you from dipping into investments that should be left to compound over longer stretches of time.

What investments should be in my cash wedge?

The investments in your cash wedge should be conservative, low-risk and easily accessible. The two most common investments that fit these criteria are guaranteed investment certificates (GICs) and bonds.

GICs are a good choice if you don't anticipate needing to take cash from your investments during the life of the GIC because those funds are locked in for that term, but rates are currently very low.

Bonds can be a less risky choice for those who need to quickly access their funds for cash. If interest rates rise after you purchase the bonds (and before they mature), you may lose some money, but it will be a relatively small amount on a short-term bond and can be managed

For example, if you invest $100,000 in a one-year bond at a 3% interest rate, and interest rates rise to 4% within that year, if you wait until maturity, you’ll still receive $103,000. But if you need to access that $100,000 after the rate increase, but before maturity, you would lose $962. The advantage is that despite the relatively small loss, you would still have access to funds you need when you need it, while the locked-in GIC would not allow for this.

Managing a cash wedge with your financial advisor

It’s obvious that if you keep taking cash out of your wedge, the wedge will eventually disappear. But it’s important to keep a wedge in place for a secure source of income during market volatility — and for your own peace of mind!

For those who have a cash wedge in place with our advisors, we’ll take the time to review your portfolio regularly — typically once a quarter. If your stock portfolio has grown, we can sell some stocks and put that profit into the cash wedge to help make up for any withdrawn cash. If the stocks haven’t grown, we won’t sell them. Instead, we’ll wait for them to grow. And when they do, we’ll replenish the cash wedge.

Of course, this is a very simple look at what can be a complex strategy. If you’re interested in using the cash wedge strategy in your portfolio (if you aren’t already), schedule a meeting with one of our advisors to find out more.